Introduction

Phenolic resins – past, present and future…

…has a renaissance arrived for the first-ever synthetic polymer?

Paul Ashford, Anthesis-Caleb

Regulatory and marketing advisors to the European Phenolic Resins Association (EPRA)

An enviable past

It’s already over ten years ago that the phenolic resins community celebrated the centenary of a Belgian national, Leo Hendrik Baekeland discovering the societal value of reacting phenol with formaldehyde to form a phenolic resin. The event was marked in September 2007 by a symposium organised by the University of Ghent which was the place where Baekeland completed his doctorate and taught for several years.

The European phenolic resins industry was well represented at the event which was partially sponsored by both the European Phenolic Resins Association (EPRA) and the then newly-formed Global Phenolic Resins Association (GPRA).

The European phenolic resins industry was well represented at the event which was partially sponsored by both the European Phenolic Resins Association (EPRA) and the then newly-formed Global Phenolic Resins Association (GPRA).

However, what has become of the technology which Baekeland had invented after he sold it to Union Carbide on his retirement in 1938? This article seeks to explore that question and highlight where phenolic resins might be going in future.

Jack of all trades…

There are significant advantages to being “first on the block”! Bearing in mind that there had been naturally sourced resins (e.g. Shellac) for many years prior, there were already well-established markets for the product. However, not even Baekeland could have predicted the breadth of application for which his invention ‘Bakelite’ was to become used – particularly when used in the form of a moulding powder.

“A thousand uses” was probably no exaggeration as the introduction of ‘Bakelite’ coincided with the burgeoning growth of demand for electrical goods as well as more traditional items such as cookware.

Today, it seems rather ironic that the sheer success of ‘Bakelite’ has caused it to be associated with a by-gone age even to the point that it has more recently been an icon of the ‘retro’ movement. However, far from being a thing of the past, phenolic resins were only just beginning to have their real potential recognized.

On the basis of these core activities the use of phenolic resins has grown consistently through the decades following sale of Baekeland’s business to Union Carbide. Demand has varied according to region, with probably the best example being the dominance of the plywood adhesives use in North America where timber-framed building techniques remain prevalent and highly reliant on stable and water-resistant binders.

On the basis of these core activities the use of phenolic resins has grown consistently through the decades following sale of Baekeland’s business to Union Carbide. Demand has varied according to region, with probably the best example being the dominance of the plywood adhesives use in North America where timber-framed building techniques remain prevalent and highly reliant on stable and water-resistant binders.

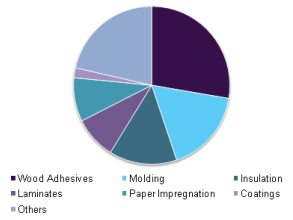

According to a range of market research sources, the global market for phenolic resins had reached close to 5 million tonnes in 2015 with a value in excess of $10 billion. Use patterns were estimated to be as follows:

More importantly, most market assessments have been predicting a CAGR of >5% in the period through to 2021, indicating that core market fundamentals for the industry remain strong.

Trade between regions usually represents less than 10% of total demand, reflecting the fact that it is not usually considered cost-effective to transport resins (particularly liquid resins) over long distances. Therefore, regional production closely parallels demand in most cases. Where leading-edge technology is required all around the world (e.g. in friction materials or rubber reinforcing resins), it has been common-place to see licensing agreements springing up to accommodate such transfer. However, in more recent years, a number of truly global manufacturers have emerged and these are able to transfer technologies internally.

At the regional level, EPRA’ own data supports the global trends observed by the market researchers. The Association covers over 90% of the European non-captive market with the exception of foundry resins. Based on its detailed statistics gathering, EPRA reports a market of over 800,000 tonnes/annum with overall activity up 6.1% in 2017. Particularly strong growth has been reported in the construction sector with mineral wool binders up 7%, wood binders up 8.2% and insulation foam resins up 13.3%, albeit from a lower base.